Key Takeaways

- Staffing accounting is its own discipline. The cash gap between weekly payroll and 30 to 60 day client receivables is the central financial problem of the industry, and it shapes everything else about how the books should be run.

- Generic CPAs miss the metrics that matter. Gross margin per assignment, DSO, spread per hour, and contractor utilization predict profitability better than revenue and net income.

- Worker classification (W-2 vs. 1099) and multi-state payroll tax exposure are the two compliance areas where a single mistake can cost six figures.

- Most agencies between $5M and $50M in revenue benefit from outsourcing day-to-day accounting, payroll, and billing to a staffing-specialized firm rather than building it in-house.

If you own a staffing firm, you already know your business runs differently than the ones your accountant probably learned in school. You pay your contractors every Friday. Your clients pay you in 45 days, sometimes 60. Your gross margin lives or dies on a markup that fluctuates by client. You manage W-2 employees, 1099 contractors, and sometimes both for the same person across different assignments. Your back office is not a department. It is the engine that determines whether you make payroll next week.

And yet most staffing owners are working with a CPA who treats them like any other small business. Quarterly check-ins. A trial balance. A tax return in April. The numbers technically reconcile, but they don’t tell you anything you can act on.

This guide is for owners who are tired of that. According to the U.S. Bureau of Labor Statistics, the temporary help services industry (NAICS 561320) employs millions of workers across thousands of firms in the United States. Yet very few of those firms are working with accounting partners who understand the industry’s mechanics. This guide walks through what accounting for a staffing agency actually looks like when it’s done right, the financial mechanics that make staffing different from every other industry, the metrics that predict whether your firm is healthy, and how to decide whether you should keep accounting in-house or hand it to a specialist.

What Makes Accounting for a Staffing Agency Different

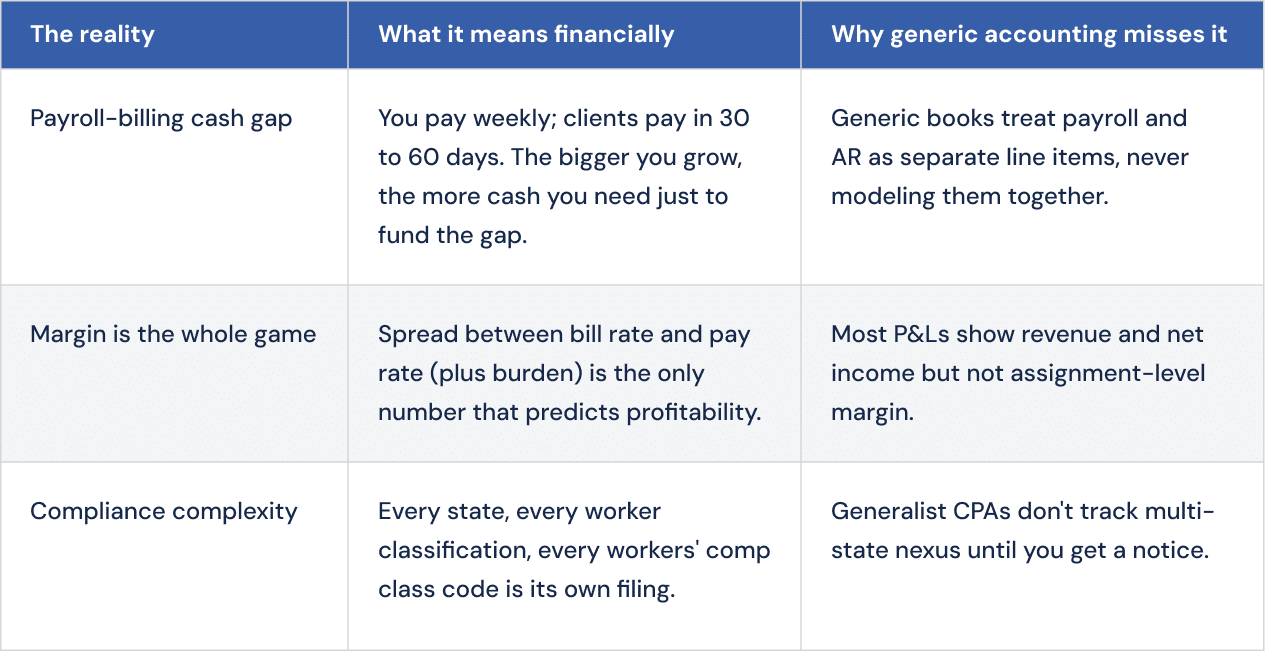

Three structural realities define staffing finance. If your CPA cannot speak to all three without you explaining them, you have the wrong CPA.

1. The payroll-billing cash gap

This is the single most important financial fact about a staffing agency. You owe your contractors money every week. Your clients owe you money every 30 to 60 days. The bigger your firm grows, the more cash you need to fund that gap, even if every assignment is profitable on paper.

A $10M staffing firm running 30-day terms is, on average, carrying about $800,000 in receivables at any given time. At 45-day terms it’s $1.2M. That money has to come from somewhere: operating cash, a line of credit, or a payroll funder like Tricom or Madison. Generic accounting doesn’t model this. Staffing accounting has to.

2. Gross margin is the whole game

In most industries, you watch revenue and net income. In staffing, those numbers are misleading. You can grow revenue 40% in a year and make less money than you did the year before, because gross margin compressed two points across your top three clients. The number that actually matters is the spread between what the client pays you per hour and what it costs you to put the contractor in the seat (including burden such as payroll taxes, workers’ comp, and benefits).

A specialized accounting services for staffing agencies team tracks gross margin at the assignment, client, and recruiter level, not just the firm level. That’s how you find out which clients are quietly destroying your profitability.

3. Compliance complexity multiplies fast

A 50-person staffing agency operating in three states has more payroll tax exposure than a 200-person professional services firm operating in one. Every state has its own unemployment insurance rate, its own workers’ comp class codes, its own filing schedule. Add 1099 contractors and the worker classification rules from the IRS and the U.S. Department of Labor, and the surface area for compliance mistakes is enormous.

This is the part of staffing finance where one error compounds. A misclassified worker isn’t just a back-tax issue. It can trigger penalties, interest, and audit exposure that cascade across years.

The Core Components of Staffing Agency Accounting

Every staffing firm’s accounting function needs to handle five things. Most owners are doing some of them well and some of them poorly without realizing which is which.

Payroll for a contractor workforce

Staffing payroll runs weekly, sometimes more often. It has to handle timecards from multiple sources, mixed worker classifications, multi-state withholding, garnishments, benefits deductions, and PTO accrual rules that vary by client contract. It also has to integrate cleanly with your billing, because the same timecard that pays the contractor invoices the client. Payroll for staffing firms done right is invisible: contractors get paid on time, every time, and you never have to think about it.

Billing tied to timecards

Client invoicing in staffing is fundamentally a timecard problem. Late timecards mean late invoices, which mean late payments, which strain cash. Bad timecard data (wrong rates, wrong markups, wrong client codes) produces invoices that get disputed and aged. Good billing services for staffing firms close the loop between timecard, invoice, and cash receipt within days, not weeks.

Accounts receivable management

Once an invoice is out, the work isn’t done. It’s just starting. Staffing firms typically need a dedicated process for AR follow-up: aging review, collections outreach, dispute resolution, and credit risk assessment for new clients. Most owners don’t have this until they get burned by a non-paying client; by then it’s already a write-off.

Accrual-based financial reporting

Cash-basis accounting hides the truth in staffing. Because of the payroll-billing gap, your cash position never matches your real economics. As the Small Business Administration explains, accrual-method accounting recognizes revenue when it’s earned and expenses when they’re incurred, regardless of when cash changes hands. For staffing, this is essential. Often this is done on a 4-4-5 calendar, which matches how staffing weeks actually fall, giving you a clean view of revenue, expenses, and margin in the period they were earned. Without it, you can’t make a real pricing decision, can’t evaluate a recruiter’s book, and can’t tell your lender or your investor what’s actually going on.

Tax planning, not just tax filing

Filing the return is table stakes. Tax planning means structuring your S-corp election, your owner compensation, your equipment purchases, and your year-end timing to legally minimize what you owe. For a staffing owner, this also means understanding federal employment tax obligations, how the R&D credit can apply to recruiter productivity tools, how the QBI deduction interacts with W-2 compensation, and how multi-state nexus changes your tax footprint.

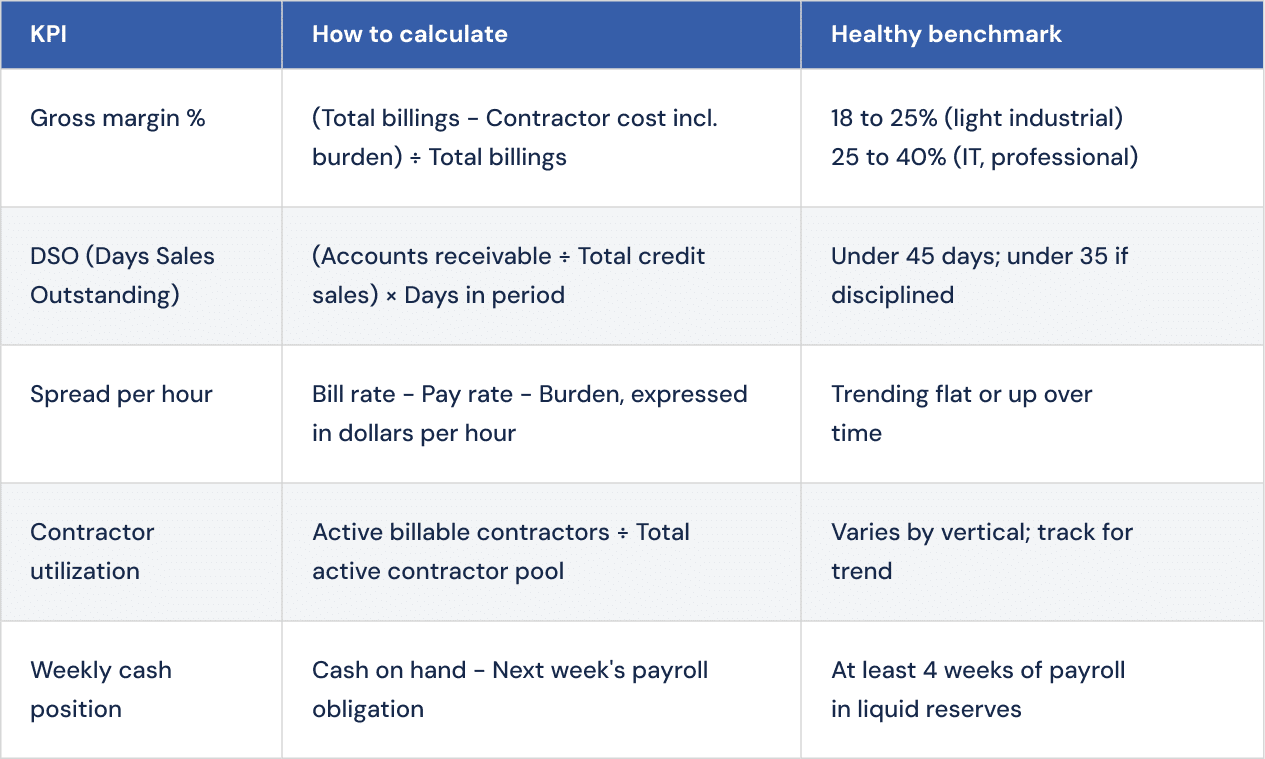

Five KPIs Every Staffing Owner Should Track Monthly

Most staffing owners can tell you their revenue and their headcount. Far fewer can tell you their gross margin trend over the last six months by client. These five metrics, reviewed every month, are the difference between running your firm by feel and running it by data.

A specialized accounting team will produce these numbers as a matter of course every month. A generalist accountant typically will not even know to ask for them.

The Compliance Issues That Actually Hurt Staffing Firms

Worker classification: W-2 vs. 1099

This is the single most expensive mistake in staffing finance. The IRS, the Department of Labor, and most state agencies have been steadily tightening the criteria for legitimate 1099 classification, and staffing is one of the highest-scrutiny industries. The IRS evaluates classification across three categories: behavioral control, financial control, and the relationship of the parties. The DOL’s Fair Labor Standards Act final rule, effective March 11, 2024, applies a six-factor economic reality test.

If you classify a worker as 1099 when the working relationship looks more like W-2, you can be liable for:

- Back payroll taxes (federal income tax, Social Security, Medicare)

- Federal and state unemployment contributions

- Workers’ comp premiums you should have been paying

- Benefits restitution if the worker should have qualified for company plans

- Penalties and interest, often calculated back several years

The fix is not to guess. It’s to apply the actual classification tests on every assignment and document the analysis. A staffing-specialized CPA does this as a matter of course.

Multi-state payroll tax

If you have contractors working in more than one state, you almost certainly have nexus, meaning you have to register for state income tax withholding, unemployment insurance, and sometimes workers’ comp in each state where work is performed. Each registration has its own filing schedule, its own rate calculation, and its own penalty structure for missed deadlines. Most generic accountants don’t track this until you get a notice.

Workers’ compensation classification

Workers’ comp premiums are calculated by class code, and the same contractor can fall into different class codes depending on the work being performed. Misclassification (or just using the wrong code by default) can mean overpaying premiums by tens of thousands of dollars a year, or underpaying and getting hit with an audit adjustment plus penalties.

Sales tax on staffing services

A handful of states tax staffing services as taxable services rather than treating them as exempt labor. The rules differ by state and by service type (light industrial often handled differently than professional services). If you’re operating in any of these states without collecting and remitting sales tax, the exposure builds quietly until an audit.

Choosing the Right Technology Stack

The right tools matter less than how well they’re integrated. A great front office (Bullhorn, TempWorks, Avionté) feeding bad data into the back office (QuickBooks, Sage Intacct) produces unreliable financials. The integration is where most agencies lose hours every week to manual reconciliation and where most reporting errors originate.

A staffing-aware accounting team should be able to:

- Implement or migrate ATS and back-office platforms without breaking financial integrity

- Map timecard data, billing rates, and pay rates cleanly between systems

- Set up reporting that pulls from both sides without manual rekeying

- Maintain audit trails that satisfy lenders, investors, and tax authorities

If your current accountant treats your tech stack as someone else’s problem, you’re carrying integration risk on your own balance sheet.

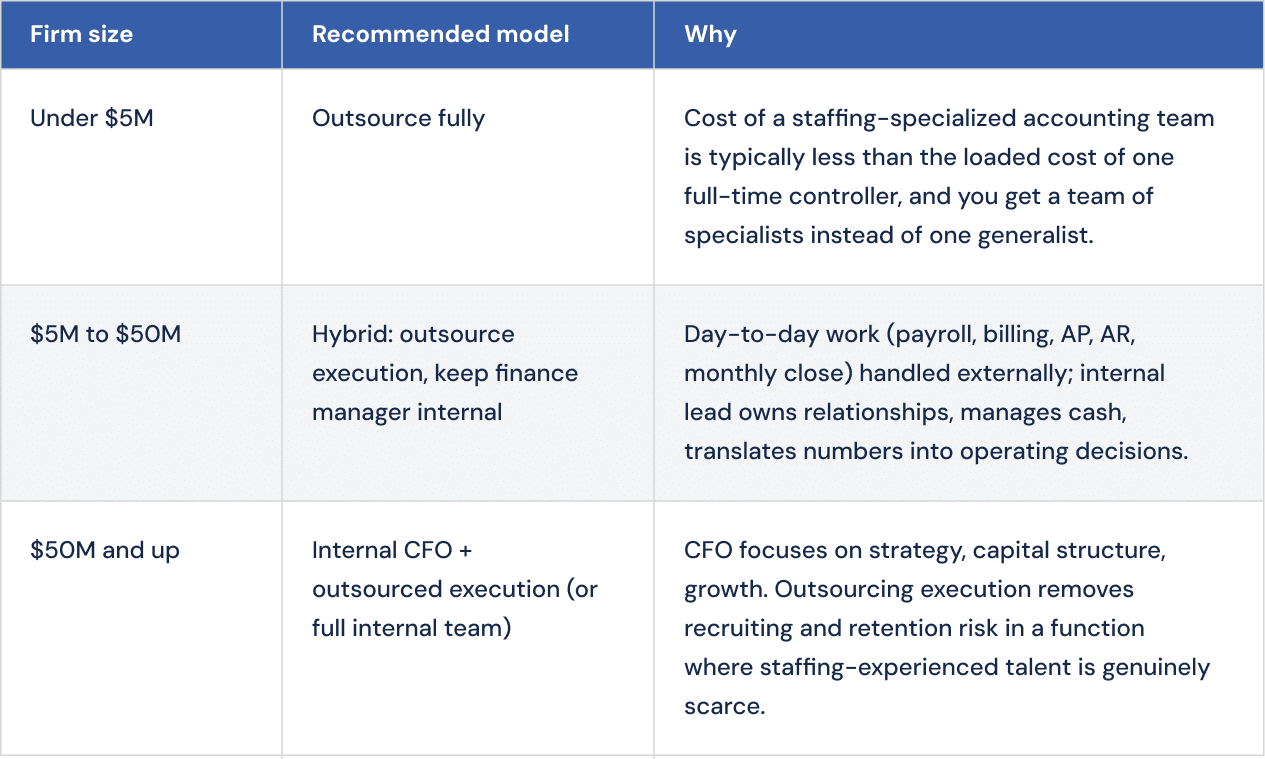

In-House vs. Outsourced Accounting: A Decision Framework

There’s no universal answer, but there is a framework most staffing owners can apply to their own firm.

This is the sweet spot for the kind of work RLP does at the $5M to $50M range. For larger firms, consultative CPA services can pair with internal finance leadership.

Signs It’s Time to Bring in a Staffing-Specialized CPA

If three or more of these describe your firm, you’re already paying the cost of generic accounting. You just don’t see it on an invoice.

- Your monthly financials arrive more than three weeks after month-end.

- You can’t tell, without pulling reports manually, what your gross margin was last month.

- You’ve been surprised by a tax bill, a payroll tax notice, or a workers’ comp audit adjustment in the last 18 months.

- Your accountant asks you basic questions about how staffing works.

- You’re considering taking on a payroll funder or expanding a credit line, and you don’t have the financials to support a clean conversation with the lender.

- You’ve outgrown the version of QuickBooks you’re on and don’t know what to upgrade to.

- Your front-office system (Bullhorn, TempWorks, etc.) and your accounting system don’t talk to each other cleanly.

The Bottom Line

Staffing is one of the most operationally complex industries to run from a financial standpoint, and one of the most rewarding when the back office is running well. The difference between a firm that stalls at $10M and a firm that scales to $50M usually isn’t sales. It’s whether the financial machinery underneath the sales engine can keep up.

Working with an accounting firm that has lived in staffing for years means you don’t have to teach anyone what a markup is, why DSO matters, or how to read a 4-4-5 calendar. You get back the time you were spending in the books, you get financials you can actually trust, and you get a partner whose job is to help you grow. Meet the team behind RLP or see what working with RLP looks like. When you’re ready to talk through whether we’re a fit, talk to our team.